Are Refiners Likely to Outperform — Even If Oil Stabilizes?

The oil and gas market is not a single trade. It is a supply chain — spanning production, refining, and distribution — with distinct segments, each moving on its own economics and timing. In the current environment, refining stands out, as margins expand into the driving season and position refiners may capture a disproportionate share of the upside.

Highlights

- In a highly volatile energy market, refining may capture a disproportionate share of the upside

- Refiners are likely to keep the windfall even if crude markets stabilize, as product pricing has historically been quick to rise and slow to normalize

- Margins are widening at the right time — peak refinery throughput into the U.S. driving season

- We have seen this dynamic before — in 2022, during the last major crude oil disruption when Russia's invasion of Ukraine shook energy markets, refining margins expanded sharply and refiners outperformed

The Disruption Is Broad — But Skews Toward Refining Margins

The recent escalation around the Strait of Hormuz — followed by a fragile de-escalation — has tightened the global energy market and pushed crude prices sharply higher. The move has been significant, and it has captured the headlines.

But the adjustment in prices is not uniform.

As the market re-prices risk across the supply chain, the impact is being distributed unevenly. Crude has moved meaningfully, but the re-accommodation of margins is skewing further downstream, where refined product prices have remained firmer even as crude begins to normalize.

That divergence is the signal, and to understand where that divergence is coming from, it helps to start with how the barrel is consumed.

Start with the Barrel: Where the Economy Buys Energy

The global economy consumes refined products, not crude oil.

Roughly:

- ~30–35% of the barrel goes to diesel and gasoil (freight, industry, heating)

- ~25–30% goes to gasoline (passenger transport)

- ~10–15% goes to jet and marine fuels (aviation and shipping)

- The balance feeds petrochemical feedstocks used to make chemicals, plastics, and many other everyday products.

This is a distillate-heavy system, and that is where constraints tend to bind.

The stress is not showing up evenly across these products.

- Jet fuel is already showing substantial price increases. It is globally traded, lightly buffered, and dependent on export flows — so it reacts first.

- Diesel is likely next. It has more inventory cover, which delays the move somewhat. But it is the deepest and tightest market, tied to logistics, industry, and heating. When it moves, price increases tend to persist.

- Gasoline prices may have substantial increases in the later phase. Gasoline prices have already begun to increase. However, the U.S. is entering the summer driving season. As demand accelerates, any residual tightness can translate into higher pricing.

This is a sequenced tightening across the barrel.

As these product markets tighten, the increase in refined product prices is redistributed across the supply chain. The allocation is not uniform — it depends on each segment’s position and constraints. Upstream producers benefit from higher crude prices, but their realization is tied to global benchmarks. Downstream distributors and end-users face higher costs, with limited ability to pass them through immediately. Across products, outcomes vary based on production flexibility, storage availability, location, and the ability of demand to adjust.

Refiners sit at the conversion point — where crude becomes usable fuel and where price divergence turns into margin. In a tightening product environment, that position becomes critical. Segments closest to that conversion bottleneck tend to capture the largest share of the adjustment.

Jet fuel and shipping fuels tend to move first — smaller, more distributed storage and continuous-flow logistics leave little buffer. Diesel follows as inventories tighten. Gasoline comes next, as seasonal demand begins to grow.

That is where the next layer of stress is likely to emerge. Gasoline is uniquely exposed to U.S. demand, which accounts for roughly a third of global consumption. As the market enters the summer driving season, demand typically rises by 5–10%, tightening the system just as refinery throughput peaks. The question is where that tightness is coming from — and how it propagates through global markets.

The Gulf Matters More Than It Looks

The Middle East plays an underappreciated role as the balancing supplier of refined products, buffering dislocations and helping stabilize global prices.

The region is typically associated with crude production, but its role in the global energy system runs deeper. Unlike most regions, which refine largely for domestic consumption, the Persian Gulf (also called the Arabian Gulf) is crucial in the Middle East for crude oil production and generally operates with a structural surplus. Local demand is limited relative to production and refining capacity, leaving a significant share of output available for export.

That surplus is what allows the region to supply the marginal barrel into global markets. The marginal barrel is the last barrel of oil needed to meet total global demand — the one that effectively sets the price because without it, supply would fall short.

Refined products — particularly jet fuel, diesel, and marine fuels — flow out of the region into deficit markets across Europe and Asia. Those flows usually move through the Strait of Hormuz, making it one of the most critical arteries not just for crude, but for finished fuels.

The scale of those flows is material. Roughly 20% of globally-traded refined products originate from the Middle East, with a disproportionate share of exportable jet fuel and middle distillates. The region’s role is even more pronounced at the margin, where incremental supply into deficit markets depends heavily on Gulf exports.

In that structure, the market is not pricing total capacity. It is pricing the availability of the balancing supply.

Even small disruptions can matter. Delays, rerouting, or higher transit costs reduce the effective availability of those marginal barrels and therefore stimulate price increases. Because the Gulf supplies the incremental barrel into global markets, any impairment there forces the adjustment elsewhere — tightening balances and supporting prices across various regions.

That is how a regional disruption propagates into global product markets.

Margins Move Without Outages

Prices move faster than barrels. Energy markets reprice risk in real time, while physical supply adjusts with a lag — prices move quickly with expectations of availability, not with the arrival of volumes. That dynamic is particularly visible in refined products.

No large-scale refinery shutdowns have been required to tighten the system. Instead, the market is responding to slower tanker flows, higher insurance costs, routing uncertainty, and precautionary inventory behavior.

For some products and regions, inventories may cover a few weeks rather than months. In key markets, commercial inventories for jet fuel and diesel typically cover 20–40 days of consumption, leaving limited buffer when supply chains are disrupted. Prices adjust first. Physical flows follow. Product prices tend to move up quickly and normalize slowly, keeping margins elevated even as crude stabilizes.

This dynamic has played out before.

Precedent: When the System Tightened, Refiners Led

The last time the market faced a comparable supply-driven shock was in 2022, in the aftermath of post-COVID dislocations and restrictions on Russian energy flows into Europe.

The system entered that period already tight. Demand had rebounded faster than refining capacity following the pandemic, while inventories remained below historical norms. The disruption of Russian crude and product exports into Europe then forced a rapid reconfiguration of global trade flows.

The adjustment showed up most clearly in refined products. Diesel markets tightened sharply, trade routes were rerouted, and inventories remained constrained. Refining margins expanded materially as product prices moved ahead of crude.

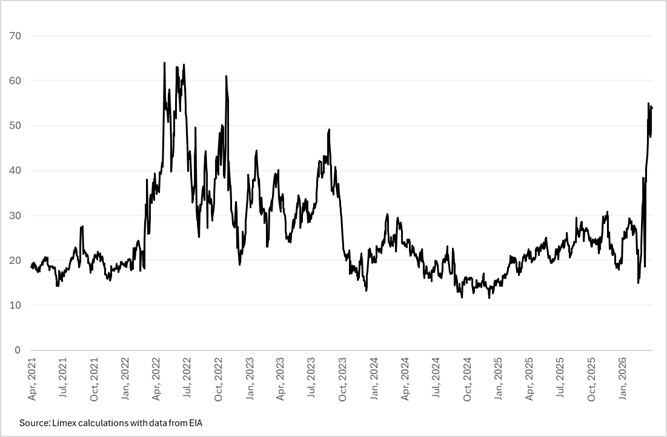

That expansion is clearly visible in crack spreads, which widened sharply during the 2022 disruption — and are now re-expanding into the current cycle.

Figure: US Refining Margins ($/bbl, 5Y)

Source: Limex calculations with data from EIA

The equity response to the supply-driven shock in 2022 followed (source: StatMuse, full year 2022):

- S&P 500: ~ -19.4% total return

- Nasdaq-100: ~ -33.1% total return

- Energy Select Sector SPDR Fund: ~ +64.2% total return

- Refiners in the S&P 500: ~ +68.3% (simple average)

Refiners outperformed both the broader market and the energy sector, as margins expanded faster than crude prices.

Gabriel Salas is a Senior Advisor to Lime Fintech, LLC and is not a representative of Lime Trading Corp. Articles written by Mr. Salas are provided by Lime Fintech, LLC, a separate but affiliated third-party. Lime Trading Corp. does not endorse or recommend products or services provided by third parties, makes no representation, and assumes no liability for the accuracy or completeness of third-party products or services.

© 2026 Securities are offered by Lime Trading Corp., member FINRA, SIPC, & NFA. Past performance is not indicative of future results. All investing incurs risk including, but not limited to, the loss of principal. Additional information may be found on our Disclosures Page. The material in this communication is not a solicitation to provide services to customers in any jurisdiction in which Lime Trading is not approved to conduct business. The material in this communication has been prepared for informational purposes only and is based upon information obtained from sources believed to be reliable and accurate; however, Lime Trading Corp. does not warrant its accuracy and assumes no responsibility for any errors or omissions. The information provided is not an offer to sell or a solicitation of an offer to buy any security or commodity or other financial product and is not a recommendation to follow a specific trading strategy. Lime Trading Corp. does not provide investment advice. This material does not and is not intended to consider the particular financial conditions, investment objectives, or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.