The Inflation Pipeline Is Increasing Pressure on the Fed

Highlights

- Headline inflation still looks manageable, but the underlying inflation pipeline is re-accelerating materially beneath the surface.

- The goods side of PPI increasingly suggests inflation pressures may be evolving from a temporary energy shock into a broader and potentially more persistent process.

- Producer-price increases are progressively moving downstream from bulk commodities into intermediate production, freight, manufacturing inputs, which may indicate inflation pressure is becoming more broadly distributed throughout the economy.

- The Fed may be less inclined to wait for inflation pressures to dissipate on their own if producer-price inflation continues moving downstream through the economy.

- Unless the Hormuz situation is resolved within days rather than months, the likelihood of meaningful rate cuts in 2026 may continue to diminish. While rate hikes remain a marginal scenario rather than the base case, even serious discussion around hikes could pressure equities, valuations, and duration-sensitive assets.

Headline inflation still looks uncomfortable, but not catastrophic. A 3–4% CPI environment is hardly good news for the Fed, but it still leaves room for the soft-landing narrative to survive. A key concern lies beneath the surface, where several leading indicators have continued to strengthen.

The first important shift is moving the focus away from CPI and toward PPI. Consumer inflation tells us where prices have already arrived. Producer inflation tells us where pressures are still moving through the system before reaching consumers. In that sense, PPI can serve as an early indicator of potential inflation persistence.

The second distinction is between goods and services inflation. Goods prices usually react first to changes in commodities, energy, freight, transportation, and manufacturing costs. Services inflation tends to follow later because it depends more on wages, labor markets, household balance sheets, and inflation expectations. Put differently, goods inflation is primarily cost-driven, while services inflation is typically more demand- and liquidity-driven.

That matters because much of the current inflation pressure appears concentrated in the physical economy.

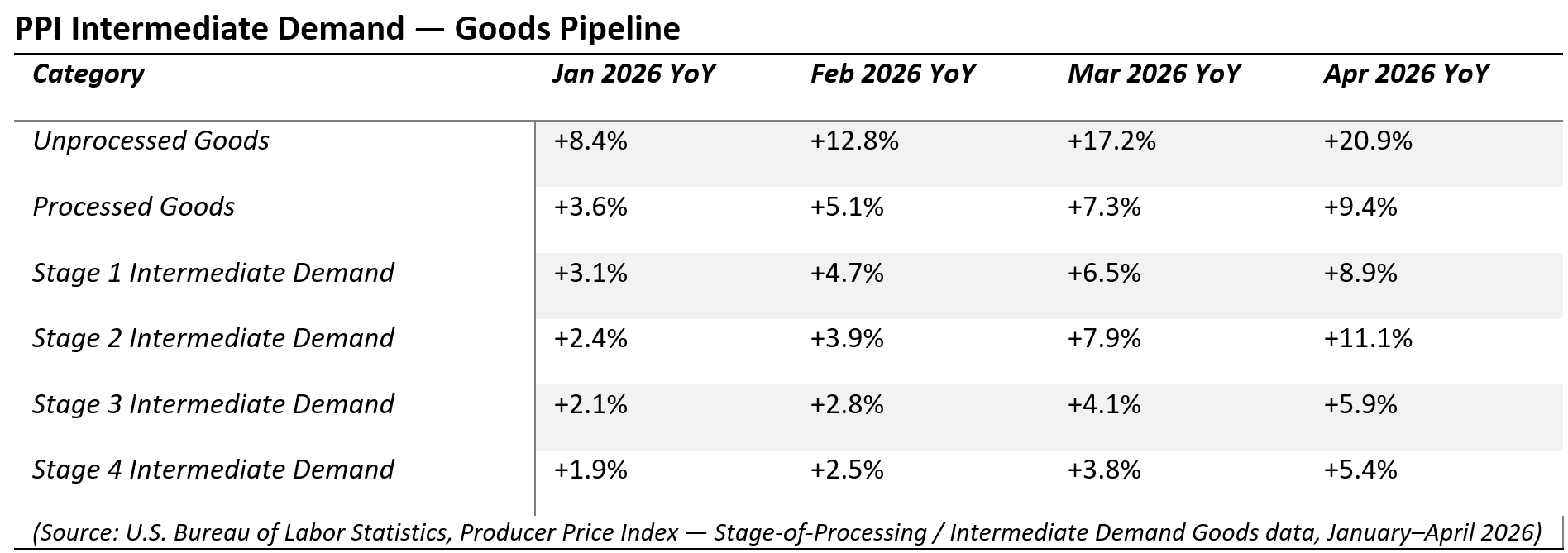

Once we isolate the goods side of PPI, the next step is tracking how inflation moves through the production chain itself. The “Stages of Intermediate Demand” framework essentially maps that progression, from upstream raw materials and crude inputs to processed industrial goods, manufacturing inputs, and eventually final demand prices.

Under normal conditions, inflation pressure dissipates as it moves downstream — from Stage 1 and Stage 2 upstream industrial inputs toward Stage 3 and especially Stage 4 goods closer to final demand. Firms absorb part of the margin pressure, consumers substitute away from expensive inputs, and supply gradually reallocates toward higher-priced goods. That is why many commodity shocks fade before embedding into broader inflation.

Energy-driven inflation behaves differently because demand elasticity is extremely low. Consumers can postpone discretionary purchases, but they cannot easily stop driving, transporting goods, heating buildings, or operating industrial systems. Refined energy products also have very limited short-term substitutes. Trucking fleets cannot quickly replace diesel, airlines cannot pivot away from jet fuel, and petrochemical supply chains cannot rapidly redesign feedstocks.

As a result, inflation pressure may not be dissipating naturally through the production chain and may instead continue transmitting downstream.

That pattern appears increasingly visible in the stage data itself.

Inflation initially appeared where expected: raw commodities, crude inputs, and energy-related goods. But instead of fading downstream, each successive stage of production has accelerated as well.

The clearest example is Stage 2, which includes refined fuels, petrochemicals, industrial chemicals, plastics, packaging, freight-linked inputs, and other energy-intensive materials. Inflation in that category accelerated from +2.4% year-over-year in January to +11.1% by April — a notable acceleration for an economy that had previously been viewed as moving toward 2% inflation.

The fuel data reinforces the concern. Retail gasoline prices rose roughly 16% from February to March and another 15% from March to April, while diesel prices followed a similar trajectory. According to AAA fuel price data, the national gasoline average rose from roughly $4.24 per gallon in April to around $4.53 as of mid-May, suggesting the first half of May continues to point higher as well, albeit at a slower pace than the sharp acceleration seen earlier in the spring. Importantly, those trends are developing just ahead of the U.S. Memorial Day holiday on May 25, traditionally considered the start of the summer driving season and historically the strongest gasoline-demand period of the year. Diesel matters particularly because its costs can affect large portions of the physical economy, including trucking, rail, agriculture, construction, logistics, and industrial production.

Current conditions may more closely resemble cost-push inflation propagating through a still-liquid economy rather than a classic demand boom. That distinction matters enormously for markets. Demand-driven inflation can usually be cooled with higher rates. Supply-chain and energy-driven inflation, however, can persist longer and may place additional pressure on margins while increasing stagflationary risks.

This is also reshaping the rates outlook for 2026.

At the start of the year, markets expected multiple Fed cuts during the second half of 2026 as inflation normalized and growth slowed. That view appears to be fading as market expectations evolve.

The combination of re-accelerating core CPI, sequential PPI increases, rising fuel costs, and broader inflation pressure may complicate the Fed’s ability to justify an easing cycle in the near term.

More importantly, market discussions increasingly appear to be shifting from:

“when do cuts begin?”

toward:

“what happens if inflation re-accelerates further?”

Rate hikes by the fall are still a marginal scenario, not the base case. But unlike a few months ago, they are increasingly being discussed as a possible scenario.

That alone matters for markets.

Historically, equities have often been more resilient during periods of slower growth when rates are falling, while persistent inflation and restrictive policy environments have at times created additional market pressure.

Markets can absorb shocks.

What they struggle with is inflation persistence.

And right now, several leading indicators suggest the economy may be transitioning from a temporary energy shock toward a more persistent inflation environment.

Gabriel Salas is a Senior Advisor to Lime Fintech, LLC and is not a representative of Lime Trading Corp. Articles written by Mr. Salas are provided by Lime Fintech, LLC, a separate but affiliated third-party. Lime Trading Corp. does not endorse or recommend products or services provided by third parties, makes no representation, and assumes no liability for the accuracy or completeness of third-party products or services.

© 2026 Securities are offered by Lime Trading Corp., member FINRA, SIPC, & NFA. Past performance is not indicative of future results. All investing incurs risk including, but not limited to, the loss of principal. Additional information may be found on our Disclosures Page. The material in this communication is not a solicitation to provide services to customers in any jurisdiction in which Lime Trading is not approved to conduct business. The material in this communication has been prepared for informational purposes only and is based upon information obtained from sources believed to be reliable and accurate; however, Lime Trading Corp. does not warrant its accuracy and assumes no responsibility for any errors or omissions. The information provided is not an offer to sell or a solicitation of an offer to buy any security or commodity or other financial product and is not a recommendation to follow a specific trading strategy. Lime Trading Corp. does not provide investment advice. This material does not and is not intended to consider the particular financial conditions, investment objectives, or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.